Most drivers assume liability insurance covers all damages after a car accident, but that’s not always true. Insurance companies have strict rules on what they will and won’t pay for, and many accident victims pay out of pocket without even realizing it.

What exactly does liability insurance cover in a car accident? And what can you do if it’s not enough? Protect yourself from costly surprises by understanding what you’re entitled to after an accident.

What Is Liability Coverage Insurance?

Liability insurance is mandatory in California and covers injuries and property damage caused by a driver in an accident. It ensures that if someone causes a crash, their insurance helps pay for the victims’ losses—including medical bills, lost wages, and car repairs.

However, liability insurance only covers other people’s damages—not the at-fault driver’s. If another driver crashes into you, their liability insurance should cover your medical expenses and vehicle repairs. But if you cause an accident, your injuries and car repairs won’t be covered—unless you have additional insurance, such as collision coverage or medical payments coverage.

Liability insurance helps protect accident victims by covering two main types of damages: bodily injury and property damage. Here’s what each type includes:

1. Bodily Injury Liability Coverage (BI): Pays for injuries caused to other people in the accident including:

- Medical expenses (ER visits, surgery, rehab, medications)

- Lost wages if the injured person is unable to work

- Pain and suffering from physical and emotional distress

2. Property Damage Liability Coverage (PD): Covers damage to someone else’s property, such as:

- Vehicle repairs or replacement

- Damage to fences, buildings, or other structures

What Does Liability Insurance NOT Cover in a Car Accident?

Many assume that auto liability insurance covers all accident-related costs, but that’s not the case. Liability car insurance only pays for other people’s injuries and property damage if the insured driver is at fault. It does not cover the insured driver’s expenses.

If you’re injured from a car accident, it’s important to understand what auto liability coverage won’t pay for—and what other options you may have for compensation. If the at-fault driver’s insurance isn’t enough, you may need to file a claim under your policy or take legal action.

Let’s break down what liability insurance does not cover and how to protect yourself.

- Won’t cover the at-fault driver’s injuries – If you cause an accident, liability insurance won’t pay for your medical bills. You’ll need personal medical coverage.

- Won’t cover the at-fault driver’s vehicle repairs – Damage to your car isn’t covered; you need collision coverage.

- Won’t cover damages beyond the policy limits – If accident costs exceed the coverage, the at-fault driver may have to pay out of pocket.

- Won’t cover hit-and-run accidents – If the at-fault driver flees the scene, liability insurance won’t help. This is why uninsured motorist (UM) coverage is essential.

Recommended Reading: Protecting Your Claim From Insurance Fraud Car Accidents

Do California Drivers Need to Carry Liability Insurance?

California requires all drivers to carry liability insurance coverage for injuries and property damage in an accident. However, the minimum liability insurance limits are often insufficient to cover all expenses from a severe accident.

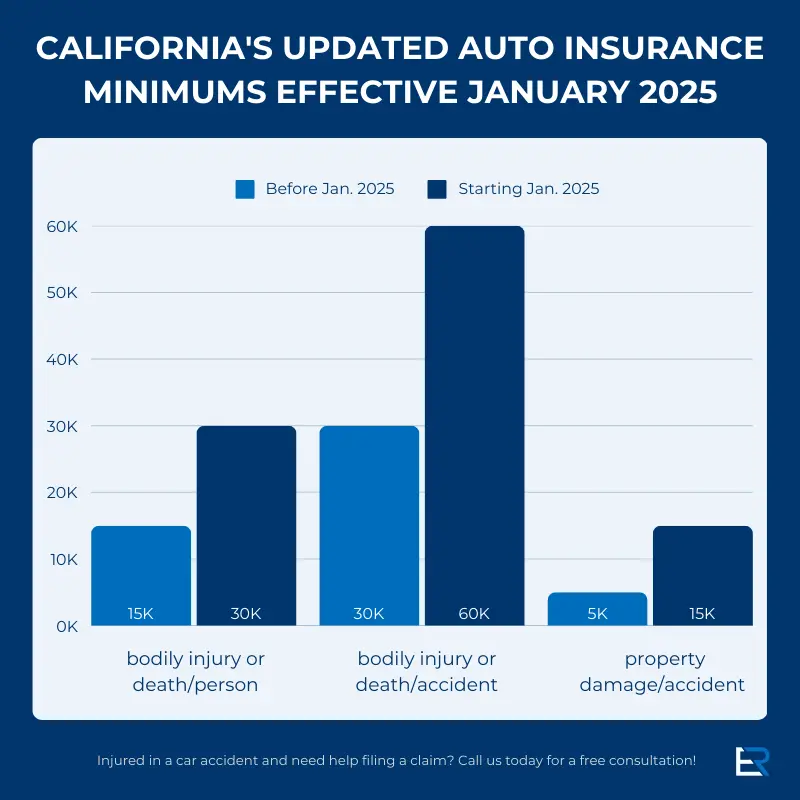

The state’s minimum liability requirements are:

- $30,000 bodily injury per person

- $60,000 bodily injury per accident

- $15,000 for property damage

Medical bills, lost wages, and car repairs can easily exceed these limits, leaving accident victims struggling to cover the remaining costs. If the at-fault driver’s insurance isn’t enough, they could be personally liable for paying the difference—or face a lawsuit.

Drivers who fail to carry insurance may face fines, license suspension, and full financial liability for any damages they cause. If an uninsured or underinsured driver has injured you, we can help you explore your legal options—call us for a free consultation!

Recommended Reading: What Happens If the Driver Isn’t Listed on the Insurance Policy?

Who Pays for Damages After a Crash in California?

California is an at-fault state, meaning the driver who caused the accident is responsible for damages. However, the state also follows a comparative negligence rule, meaning if you are partially at fault, your compensation may be reduced by your percentage of fault.

If you’re injured in a crash, you can recover compensation for damages by:

- Filing a claim with the at-fault driver’s insurance.

- Filing a lawsuit against the at-fault driver.

What Can You Recover After an Accident?

If you’ve been injured in a car accident, you may be entitled to compensation for:

- Economic Damages: Medical bills, lost wages, and property damage.

- Non-Economic Damages: Pain and suffering, emotional distress, and permanent injuries.

- Punitive Damages: Awarded in extreme cases, such as DUI accidents.

Don’t settle for less than you deserve. Our personal injury lawyer can negotiate maximum compensation while you focus on recovery. Schedule a free consultation with El Dabe Ritter Trial Lawyers today!

What If the Crash Involved a DUI or Other Crime?

Sometimes a car accident is caused by criminal conduct, such as drunk driving, reckless driving, or street racing. In these situations, the at-fault driver may face criminal charges in addition to a civil insurance claim.

California’s Marsy’s Law gives crime victims important rights during the criminal process and may allow restitution for certain out-of-pocket expenses. However, a criminal case is designed to punish the offender, not fully compensate accident victims.

To recover compensation for medical bills, lost wages, property damage, and pain and suffering, you will typically need to pursue a separate personal injury claim against the driver’s liability insurance. Evidence from the criminal case, such as police reports, toxicology results, and witness statements, can often strengthen your insurance claim and help establish fault.

What If the At-Fault Driver Doesn’t Have Enough Liability Insurance?

Unfortunately, many drivers in California are uninsured or underinsured, meaning they are driving illegally without proper coverage. If the at-fault driver doesn’t have enough insurance to pay for your damages, you may still have options:

- Uninsured Motorist (UM) Coverage: Pays for your injuries if the at-fault driver has no insurance.

- Underinsured Motorist (UIM) Coverage: Covers damages that exceed the at-fault driver’s policy limits.

- A personal injury lawsuit: You may be able to sue the at-fault driver for damages.

Recommended Reading: Do I Have a UM/UIM Case?

What to Do After a Car Accident to Protect Your Claim

The steps taken after a car accident can make or break your claim. Insurance companies look for any reason to deny or reduce your payout—here’s how to protect your rights from day one.

- Call 911 – File a police report for evidence of the accident.

- Get medical attention – Some injuries may not appear right away.

- Take photos and videos – Document the accident scene with any vehicle damage, or injuries.

- Get witness information – Witness statements can help prove fault.

- Avoid admitting fault – Insurance companies can use anything you say to reduce or deny your claim.

- Call a personal injury attorney – An accident attorney in Los Angeles can help protect your rights and negotiate a fair settlement.

How a Lawyer Can Help You Recover Maximum Compensation

Dealing with insurance companies after a car accident can be frustrating. They often delay claims, offer low settlements, shift blame, or use your statements against you to reduce payouts. A skilled personal injury lawyer knows these tactics and can fight back to secure the compensation you deserve.

Here’s how a lawyer can help:

- Handle all negotiations – We push back against lowball offers and fight for full compensation.

- Prove liability – We collect evidence, accident reports, and witness statements to build a strong case.

- Calculate damages – We assess medical bills, lost wages, and future costs to ensure nothing is overlooked.

- We can take the case to trial if needed – If insurers refuse a fair settlement, we’re ready to fight for you in court.

At El Dabe Ritter Trial Lawyers, we take on the legal battle so you can focus on healing. You pay nothing upfront—we only get paid if we win.

Injured in a Car Accident? Get a Free Consultation Today!

If you were hurt in a car accident, don’t trust the insurance company to offer a fair deal. At El Dabe Ritter Trial Lawyers, we fight for the rights of injured victims. You deserve full compensation, not a lowball settlement. Our personal injury lawyers will maximize your recovery—and you pay nothing unless we win. Call us today for a free consultation and let’s get started!